If you moved to Canada in your 40s or 50s — or you've sponsored your parents to come here on PR — one question comes up fast: will we actually get a Canadian pension when we retire? The honest answer is "partly, and it depends heavily on how long you live in Canada." This guide breaks down Canada's three retirement-income pillars in plain language, with verified 2026 figures, and explains the one rule that trips up almost every newcomer family: the OAS residence requirement.

Quick Answer: How OAS, CPP and GIS Work for Newcomers

Canada has three separate senior benefits, and they follow different rules:

- OAS (Old Age Security) is residence-based. You generally need 10 years of residence in Canada after age 18 to collect it at 65 while living in Canada (20 years to keep collecting it abroad). Every year of residence builds 1/40th of the full pension.

- CPP (Canada Pension Plan) is contribution-based. You earn it by working and paying into CPP through your paycheque. No minimum residence — just contributions.

- GIS (Guaranteed Income Supplement) is an income-tested top-up for low-income seniors who already receive OAS. Sponsored immigrants generally cannot receive GIS during their sponsorship period if they've lived in Canada fewer than 10 years.

A newcomer who arrives mid-life will usually get a partial OAS and a small CPP — proportional to their years here and their contributions. That's still real money, but it's not the full pension someone who worked here their whole life receives.

Summary: Three pillars, three rule sets. OAS counts your years living here, CPP counts your contributions, and GIS tops up low-income seniors. Newcomers get partial benefits scaled to their time and work in Canada.

Pillar 1: Old Age Security (OAS) — The Residence Pension

OAS is a monthly payment from the federal government to most seniors 65 and older. You don't have to have worked to get it — it's based on how long you've lived in Canada as an adult.

The 10-year residence rule (the big one for newcomers)

To receive OAS while living in Canada, you must:

- Be 65 or older,

- Be a Canadian citizen or legal resident, and

- Have lived in Canada for at least 10 years after turning 18.

To keep receiving OAS after you move abroad, the bar is higher: at least 20 years of residence in Canada after age 18.

Full vs. partial OAS

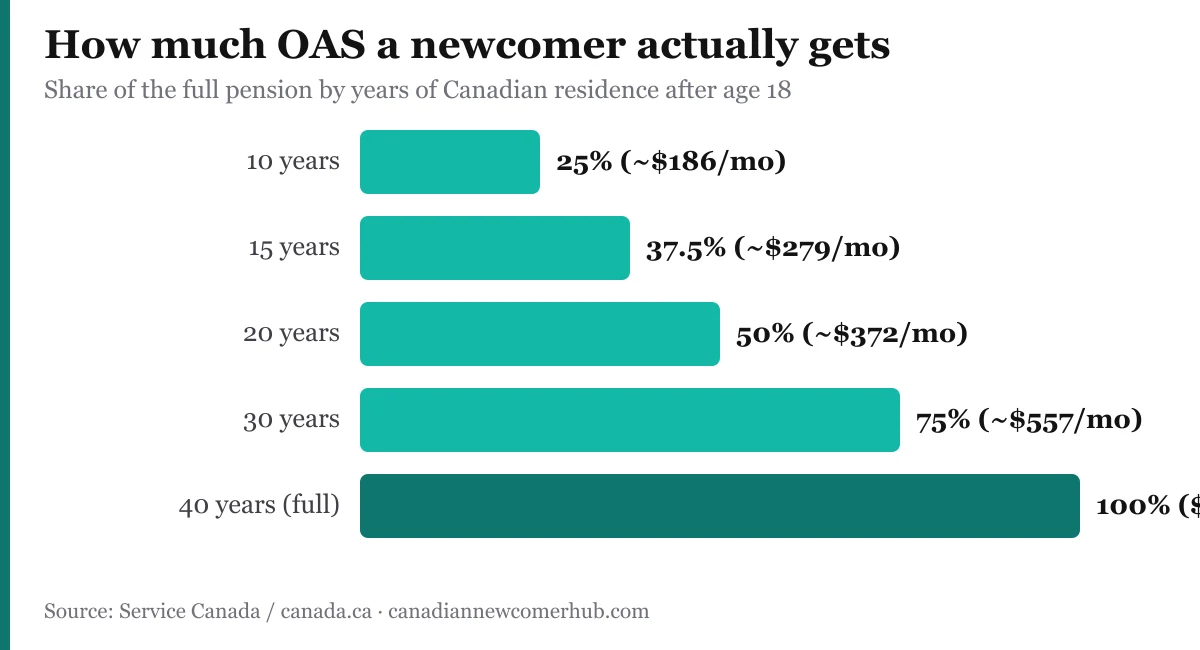

OAS is built in fortieths. 40 years of Canadian residence after 18 = the full pension. Fewer years = a partial pension prorated to your years here.

A practical example: a newcomer who lands at 50, lives in Canada continuously, and applies at 65 has 15 years of residence — so they'd qualify for roughly 15/40 (about 37.5%) of the full OAS. Someone who arrives at 55 and reaches the 10-year minimum at 65 would get 10/40 (25%).

2026 OAS amounts

OAS is adjusted quarterly for inflation. For the April to June 2026 quarter, the maximum monthly OAS pension is:

| Age | Maximum monthly OAS (full, 40 years) |

|---|---|

| 65 to 74 | $743.05 |

| 75 and over | $817.36 |

Seniors 75 and older receive a permanent 10% higher OAS — a boost introduced in July 2022. Remember these are full-pension maximums; a newcomer with a partial pension receives the same percentage of these figures.

The OAS clawback (recovery tax)

High-income seniors repay some or all of their OAS through the recovery tax. For the 2025 income year, OAS starts being clawed back once your net world income exceeds $93,454, at a rate of 15 cents per dollar above that line, until it's fully recovered at the upper threshold (roughly $151,668 for ages 65–74 and $157,490 for 75+). Most newcomer seniors on a partial pension never come close to this threshold — it mainly affects high earners.

Summary: OAS rewards years lived in Canada. Hit 10 years to collect at 65, 20 to keep it abroad, 40 for the full amount. The full 2026 maximum is $743.05 (65–74) or $817.36 (75+) per month, and the clawback only bites above ~$93k of income.

Pillar 2: Canada Pension Plan (CPP) — The Work Pension

CPP works completely differently from OAS. It's a contributory plan: while you work in Canada, you and your employer each pay CPP on your earnings (it shows up as a deduction on every payslip). When you retire, CPP pays you back based on how much and how long you contributed.

Key points for newcomers:

- No minimum residence. Even one year of CPP contributions earns you a (small) future CPP benefit. This is good news — your working years here are never "wasted."

- You can start CPP as early as 60 (reduced) or as late as 70 (increased). The standard age is 65.

- The more years you contribute near the maximum pensionable earnings, the larger your pension.

2026 CPP amounts

For 2026, the maximum monthly CPP retirement pension starting at 65 is $1,507.65. But almost no one gets the max — it requires close to 40 years of near-maximum contributions. The average new CPP retirement benefit is far lower (around $900 a month). A newcomer who works in Canada for, say, 15 years at a moderate salary should expect a modest CPP — meaningful, but well below the maximum.

CPP also includes disability, survivor, and children's benefits, all tied to your contribution record. To work and contribute, you first need a Social Insurance Number — see our guide on how to apply for a SIN in Canada.

Summary: CPP is earned, not granted. Every year you work and pay into it counts, with no residence minimum — but a mid-life arrival realistically collects a modest CPP scaled to their contribution years.

Pillar 3: Guaranteed Income Supplement (GIS) — The Low-Income Top-Up

GIS is a monthly, non-taxable top-up for low-income seniors who already receive OAS. It's income-tested: the lower your income, the more GIS you get; above a cutoff, you get nothing.

2026 GIS amounts (approximate, Q1 2026)

| Situation | Maximum monthly GIS |

|---|---|

| Single, widowed or divorced | about $1,105 |

| Married/common-law (both receive OAS) | about $665 each |

GIS amounts adjust every quarter, and the exact figure drops as your other income rises. Income thresholds are roughly under $22,000 (single) to qualify.

The catch for sponsored immigrants

This is critical for families who sponsored parents or grandparents to Canada. Since October 1, 2025, sponsored immigrants generally cannot receive GIS for the entire duration of their sponsorship (20 years in most provinces, 10 in Quebec), regardless of how long they have lived in Canada. The federal sponsorship undertaking (20 years in most provinces, 10 in Quebec) means the sponsor is legally responsible for the parent's financial needs — so the government doesn't pay the income-tested GIS on top.

In practice, a sponsored parent who arrives at 60 may qualify for a partial OAS at 65 (once they hit 10 years of residence at age 70), but GIS stays off the table for the full sponsorship period (typically 20 years from landing), not merely until the 10-year residence mark. If you're still planning a parent's arrival, the Super Visa for parents and grandparents is a common alternative to permanent sponsorship.

Summary: GIS helps the lowest-income seniors, but sponsored newcomers with under 10 years here usually can't claim it during sponsorship. Budget for that gap when you sponsor a parent.

What a Newcomer Realistically Gets

Let's make it concrete. Three common scenarios:

- Arrived at 35, works to 65 (30 years here): ~30/40 of full OAS (about $557/month at 2026 rates) + a solid CPP from 30 working years. A comfortable public-pension base.

- Arrived at 50, works to 65 (15 years here): ~15/40 of full OAS (about $279/month) + a modest CPP. Partial, but real.

- Sponsored parent arrives at 60, no Canadian work: Reaches 10-year residence at 70 → partial OAS (~10/40 = 25%) starting then; no CPP (never contributed); no GIS while sponsored.

The pattern is clear: the later you arrive and the less you work here, the smaller your Canadian pension — which is exactly why social-security agreements matter.

Social Security Agreements: A Lifeline for Newcomers

Canada has international social security agreements with more than 50 countries (including the US, India, China, the Philippines, the UK and many EU nations). These agreements can help you in two ways:

- Qualify for OAS sooner. If you haven't reached 10 years of Canadian residence, periods of residence or contribution in your home country may be counted toward meeting the 10-year minimum — letting you qualify when you otherwise couldn't.

- Receive OAS abroad. Combined time in Canada and a treaty country can help you meet the 20-year rule for collecting OAS overseas.

Important nuance: an agreement helps you qualify, but your OAS payment is still based on your actual years of Canadian residence, not the combined total. So it opens the door — it doesn't inflate the cheque. Check whether your country of origin has an agreement with Canada before assuming you fall short.

Summary: If you're near but not at 10 years of residence, a social security agreement with your home country may let you qualify for OAS — though the payment still reflects only your Canadian years.

How and When to Apply

- OAS: Many seniors are automatically enrolled and receive a letter the year before turning 65. If you don't get one, apply through your My Service Canada Account or by paper, ideally 6 months before you want payments to start. You can defer OAS up to age 70 for a larger amount.

- CPP: Not automatic — you must apply (online or by mail). Apply a few months before your chosen start date.

- GIS: Usually applied for alongside OAS; you must keep filing your taxes every year to stay enrolled.

Filing a Canadian tax return every year is non-negotiable for these benefits — GIS in particular is recalculated from your return annually. If this is your first time, see our walkthrough on filing taxes in Canada as a newcomer.

Frequently Asked Questions

Can my sponsored parents get OAS and GIS?

Sponsored parents can qualify for a partial OAS once they've lived in Canada 10 years after age 18 and turn 65. GIS is generally not payable to sponsored immigrants for the entire sponsorship period (20 years in most provinces, 10 in Quebec), regardless of years of residence, because the sponsor is financially responsible. Plan for that gap.

I arrived at 52. Will I get any Canadian pension?

Yes — a partial one. If you live here continuously and apply at 65, you'd have 13 years of residence (about 13/40 of OAS), plus whatever CPP your working years here earn. A social security agreement with your home country may also help you qualify.

Do I need to have worked in Canada to get OAS?

No. OAS is residence-based, not work-based — you qualify by living in Canada long enough. CPP is the one that requires work and contributions.

What's the difference between OAS and CPP?

OAS is funded by general tax revenue and based on years of residence; everyone who meets the residence test gets it. CPP is funded by payroll contributions and based on what you paid in. Most retirees receive both.

Will my home-country pension reduce my Canadian benefits?

Foreign pensions don't reduce your OAS or CPP directly, but they count as income for the GIS income test and can trigger the OAS clawback if your total income is very high. Report all worldwide income on your Canadian tax return.

When should I apply for OAS?

Apply about 6 months before you turn 65 (if not auto-enrolled). You can defer up to age 70 for a permanently higher monthly amount — worth considering if you don't need the income immediately.

References

- Old Age Security — Overview, Canada.ca

- Old Age Security — Do you qualify (residence requirements), Canada.ca

- Old Age Security payment amounts, Canada.ca

- Maximum Benefit Amounts and Related Figures — CPP (2026) and OAS (April to June 2026), Canada.ca

- Old Age Security pension recovery tax, Canada.ca

- Guaranteed Income Supplement — How much you could receive, Canada.ca

- Canada Pension Plan — How much could you receive, Canada.ca

- Lived or living outside Canada — Pensions and benefits (social security agreements), Canada.ca