If you are new to Canada and even quietly thinking about buying a home one day, the First Home Savings Account (FHSA) is probably the single most generous registered account the government will hand you. It is also one of the most misunderstood — partly because it launched recently (in 2023), and partly because almost no explainer addresses the question newcomers actually have: Can I even open one if I'm here on a work permit?

The short version is yes, in many cases you can. But the rules around residency, first-time-buyer status, and contribution timing have real money attached to them, and getting them wrong can cost you deduction room or trigger a penalty tax. This guide walks through exactly how the FHSA works in 2026, who qualifies, how it stacks up against the Home Buyers' Plan and a TFSA, and the deadline mechanics that trip people up. Every figure below is verified against the Canada Revenue Agency's official pages, linked in the References section.

Quick Answer: What Is the FHSA and Should a Newcomer Open One?

The FHSA is a registered account that combines the best feature of an RRSP (contributions are tax-deductible) with the best feature of a TFSA (qualifying withdrawals are completely tax-free). You can contribute up to $8,000 per year, to a lifetime maximum of $40,000, and when you withdraw the money to buy a first home, you pay zero tax on the contributions or the growth.

No other account in Canada does both. With an RRSP you get the deduction but pay tax on withdrawal; with a TFSA you get tax-free growth but no deduction. The FHSA gives you both — which is why, if you are a tax resident of Canada with a valid Social Insurance Number and you have not owned a home you lived in recently, opening an FHSA is usually a smart move even before you are certain you'll buy. The catch is a subtle one most people miss: your contribution room only starts accumulating after you open the account, so there is a real cost to waiting.

If you are still sorting out the basics of registered accounts, our RRSP vs TFSA guide for newcomers is the natural companion to this one.

How the FHSA Works: Contribution Limits and Carry-Forward

The numbers are simple, but the timing rules are where the value hides.

- Annual limit: $8,000. This is the most you can contribute in a single calendar year, regardless of income.

- Lifetime limit: $40,000. Across all your FHSAs, total contributions can never exceed $40,000. Anything above this cannot be deducted on your tax return.

- Carry-forward: up to $8,000. If you don't max out a year, you can carry forward unused room — but only up to $8,000 into the next year. So the most you can ever contribute in a single year is $16,000 ($8,000 current + $8,000 carried forward).

Here's the rule newcomers most often get wrong: FHSA participation room starts accumulating only once you open your first FHSA. Unlike the TFSA, room does not build up retroactively for the years you were eligible but hadn't opened an account. In the year you open your first FHSA, your room is $8,000 — full stop. If you were eligible in 2024 but only open an account in 2026, you do not get $24,000 of room. You get $8,000.

This is the practical takeaway: if you qualify, there is a strong argument for opening an FHSA now — even with a $0 contribution — just to start the carry-forward clock. The account itself is free to open at most institutions.

The tax deduction works like an RRSP: contributions reduce your taxable income for the year. And like an RRSP, you don't have to claim the deduction in the year you contribute — you can carry it forward to a future year when your income (and tax bracket) is higher, which is often smart for a newcomer whose first Canadian year was only partial.

One warning: over-contributing is penalized. If you put in more than your room allows, the CRA charges a tax of 1% per month on the highest excess amount, every month until you fix it. Track your room carefully, especially if you hold FHSAs at more than one bank.

Summary: $8,000/year, $40,000 lifetime, carry-forward capped at $8,000. Room only starts when you open the account — so opening early, even empty, protects future room. Over-contributions cost 1% per month.

Who Qualifies: The Newcomer and Residency Angle

To open an FHSA, the CRA requires you to meet all of the following at the time you open the account:

- Be a resident of Canada. This means a tax resident — the test that matters is residency for tax purposes, not your specific immigration status. A temporary resident, such as a work permit holder, who has become a tax resident of Canada and holds a valid SIN, can generally open an FHSA. You don't need to be a permanent resident or citizen.

- Have a valid Social Insurance Number (SIN). If you haven't got yours yet, see our SIN application guide — it's typically your first administrative task after landing.

- Be at least 18 years old (or the age of majority in your province) and no older than 71 as of December 31 of the year you open the account.

- Be a first-time home buyer. The CRA defines this precisely: you must not have lived in a qualifying home (anywhere in the world, treated as if it were in Canada) as your principal residence that you owned or jointly owned, at any time in the current calendar year or in the previous four calendar years.

That last point carries a trap for couples. If you live with a spouse or common-law partner when you open the FHSA, their home ownership counts too. If your partner owned the home you both live in within that look-back window, you are not considered a first-time buyer — even if your name was never on the title. Both partners must clear the test independently.

For many newcomers this is actually good news. Because the four-year window only counts homes you lived in as a principal residence and owned, a property you rented out back in your home country generally does not disqualify you — but a home you lived in and owned abroad recently can. When in doubt, this is exactly the kind of question worth confirming with a tax professional before you open the account.

Summary: Tax resident of Canada + valid SIN + aged 18–71 + first-time buyer (no owned principal residence in the current or prior 4 years, including your live-in partner's). Work-permit tax residents can qualify; PR status is not required.

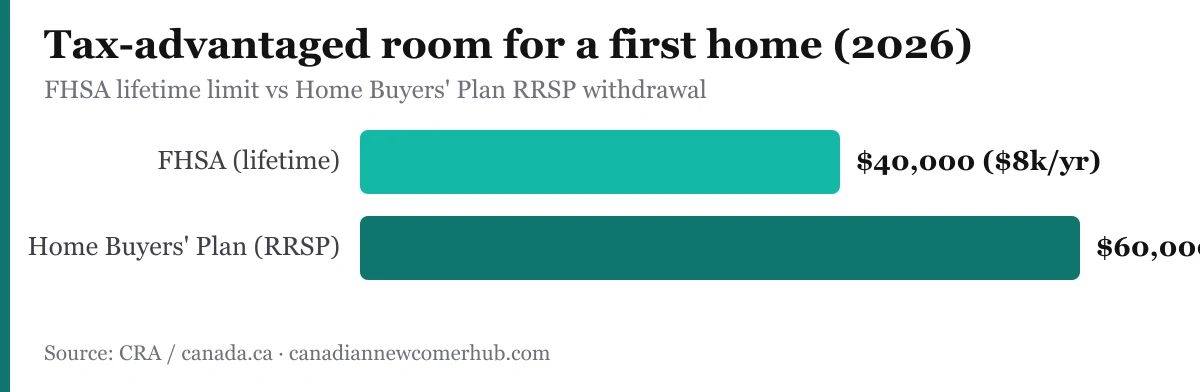

FHSA vs Home Buyers' Plan vs TFSA

These three are the tools newcomers weigh against each other. Here is how they actually differ.

| Feature | FHSA | Home Buyers' Plan (HBP) | TFSA |

|---|---|---|---|

| What it is | Standalone registered account | A withdrawal program from your RRSP | Standalone registered account |

| Contribution deductible? | Yes (like an RRSP) | Yes (the RRSP contribution is) | No |

| Withdrawal for home taxed? | No — tax-free, kept | Tax-free, but must be repaid | No |

| Max for a home | $40,000 lifetime contributions | $60,000 withdrawal | No specific limit (your room) |

| Repayment required? | No | Yes — over 15 years, or it's taxed | No |

| Must be first-time buyer? | Yes | Yes | No |

The headline difference: the FHSA is money you keep; the HBP is a loan to yourself. Under the Home Buyers' Plan you can withdraw up to $60,000 from your RRSP toward a first home, but you must repay it into your RRSP over 15 years or face tax on the shortfall. The FHSA has no repayment at all — the withdrawal is simply yours.

You do not have to choose just one. The FHSA and HBP can be combined for the same home purchase, as long as you meet each program's conditions at the time of each withdrawal. A well-prepared newcomer could draw $40,000 tax-free from an FHSA and another $60,000 from an RRSP under the HBP toward the same down payment.

Where does the TFSA fit? It has no deduction and no first-time-buyer restriction, so it's the flexible all-purpose account. The usual sequencing logic: an FHSA first if home ownership is a genuine goal (the deduction plus tax-free withdrawal is unbeatable), then a TFSA for everything else. We compare the RRSP and TFSA side by side in our dedicated guide.

Summary: FHSA = money you keep, tax-deductible going in, tax-free coming out. HBP = a $60,000 self-loan from your RRSP that you must repay over 15 years. You can use both for the same home. TFSA is the flexible backup with no first-time-buyer rule.

Where and How to Open an FHSA

FHSAs are offered by the same institutions that handle RRSPs and TFSAs: the big banks (RBC, TD, CIBC, Scotiabank, BMO), credit unions, and self-directed brokerages (Questrade, Wealthsimple, Qtrade). You can hold cash, GICs, mutual funds, ETFs, and stocks inside one, depending on the provider.

Two practical decisions:

- Savings-style vs investing-style. Big-bank "FHSA savings accounts" are simple but pay low interest. If your home purchase is several years out, a self-directed FHSA holding low-cost ETFs lets the tax-free growth actually compound. If you plan to buy within a year or two, a high-interest cash or GIC FHSA protects the principal — see our roundup of high-interest savings accounts for the rate landscape.

- Open early, fund later. Because room only starts at account opening, opening one with $0 today is a legitimate strategy purely to begin accumulating carry-forward room.

To open one you'll typically need your SIN, government ID, and proof of Canadian address. Newcomer banking packages often bundle the FHSA in with the chequing/savings setup, which is worth asking about when you arrive. For the broader sequence of money tasks in your first months, our first-year financial checklist lays it out in order.

The Deadline Mechanics That Matter

A few timing rules to keep on your radar:

- Contribution deadline is December 31, not the RRSP-style early-March deadline. FHSA contributions only count for the calendar year in which they're actually made.

- The maximum participation period is 15 years, counted from when you open your first FHSA. The account must close by December 31 of the year you turn 71, the 15th anniversary, or the year after your first qualifying withdrawal — whichever comes first.

- If you don't buy a home, the funds aren't lost — you can transfer the full balance, tax-free, into your RRSP or RRIF without using any RRSP room. That makes the downside of opening one quite small.

Summary: Open at any bank, credit union, or brokerage. Contribution deadline is December 31. The account has a 15-year (or age-71) shelf life, and unused funds roll tax-free into your RRSP — so there's little to lose by opening one.

Frequently Asked Questions

Can I open an FHSA on a work permit?

Generally yes, if you are a tax resident of Canada with a valid SIN and you meet the age and first-time-buyer rules. The CRA's test is tax residency, not permanent-resident status. If you're unsure whether you qualify as a tax resident, confirm with a tax professional before opening.

Does owning property in my home country disqualify me?

It depends on use. The first-time-buyer test looks at whether you lived in a home you owned as your principal residence in the current year or prior four years — anywhere in the world. A property you owned purely as a rental generally doesn't disqualify you, but a home you lived in and owned abroad recently can.

Can I use the FHSA and the Home Buyers' Plan together?

Yes. You can make a qualifying FHSA withdrawal and an HBP withdrawal from your RRSP for the same home, provided you meet each program's conditions at the time of each withdrawal. That's up to $40,000 from the FHSA plus up to $60,000 from the RRSP toward one purchase.

What happens if I never buy a home?

You don't lose the money. You can transfer the entire FHSA balance — contributions and growth — into your RRSP or RRIF tax-free, without using RRSP contribution room. Alternatively you can withdraw it as a taxable non-qualifying withdrawal.

How much room do I get if I was eligible for years before opening?

Only $8,000 in the year you open your first FHSA. Room does not accumulate retroactively for years before you had an account. This is why opening early, even with no contribution, is worth considering.

Do contributions have a March deadline like the RRSP?

No. FHSA contributions must be made by December 31 to count for that calendar year. There is no early-spring "first 60 days" window.

References

- First Home Savings Account (FHSA) — Canada.ca

- Participating in your FHSAs (contribution room and carry-forward) — Canada.ca

- Tax deductions for FHSA contributions — Canada.ca

- What happens if you contribute or transfer too much to your FHSAs — Canada.ca

- Withdrawals from your FHSAs (qualifying withdrawal conditions) — Canada.ca

- The Home Buyers' Plan — Canada.ca

This article is general information, not personalized tax or financial advice. FHSA and immigration rules change; verify your specific situation against the linked CRA pages or with a qualified professional before acting.