Opening a Canadian bank account is one of the very first things on a newcomer's checklist — usually right after getting a Social Insurance Number. You need an account to receive a paycheque, pay rent, and start building a credit history. The good news: all of Canada's big banks run dedicated "newcomer" programs that waive monthly fees for the first year or two and let you open an account without any Canadian credit history. The catch is that the advertised "value" numbers are marketing bundles — the actual cash you can count on, and the fine print, varies a lot between banks.

This guide compares the verified 2026 newcomer offers from the Big Five banks plus the best no-fee online banks, so you can pick the right account before you arrive.

Quick Answer: Which Newcomer Bank Account Is Best?

For most newcomers, the strongest verified 2026 offers are CIBC (up to 24 months with no monthly fee plus a $500 cash bonus for setting up direct deposit) and TD ($500 cash plus a 12-month fee rebate on Unlimited Chequing). RBC, Scotiabank StartRight, and BMO NewStart are all solid alternatives, each waiving monthly fees for at least 12 months and requiring no Canadian credit history to open. The "right" choice usually comes down to which bank has a convenient branch near you and which bonus conditions you can realistically meet.

Summary: Every Big Five bank waives chequing fees for newcomers and asks for no credit history. CIBC and TD currently offer the clearest cash value; pick based on branch access and whether you can meet the direct-deposit or spend conditions.

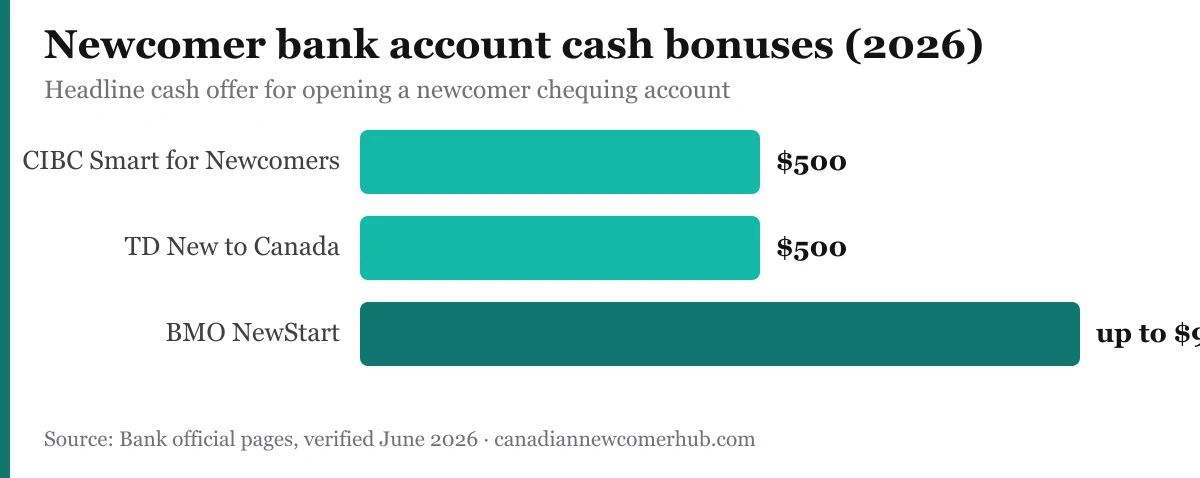

Comparing the Best Newcomer Bank Packages (2026)

The big banks bundle a chequing account, a credit card, and sometimes a savings rate into one "newcomer program." Below are the headline, verified terms. Cash bonuses almost always require a qualifying action (a direct deposit or a minimum spend) — read each bank's terms before assuming you'll get the full advertised amount.

| Bank | Program | Chequing fee waiver | Headline cash/bonus | Eligibility window |

|---|---|---|---|---|

| CIBC | Smart Account for Newcomers | Up to 24 months no fee | $500 (set up direct deposit) | Landed immigrant/PR within last 5 years, or temporary resident with a Canadian work permit issued for ≥12 months |

| TD | New to Canada Banking Package | 12 months on Unlimited Chequing | $500 cash (by Oct 1, 2026) | Newcomers to Canada |

| RBC | Newcomer Advantage | 12 months on Advantage Banking | Up to 12% cash back on Cash Back Mastercard (3 months) | PR/student ≤12 mo; worker ≤48 mo |

| Scotiabank | StartRight | 12 months on Preferred Package | 40,000 Scene+ points (Passport Visa Infinite sign-up; $2,000 spend in 3 months) | PR/student/worker, 0–5 years |

| BMO | NewStart | 24 months on Performance Plan | Up to $900 + perks | Arrived within last 5 years |

A few things to note:

- CIBC stands out for its fee waiver length — up to 24 months with no monthly fee and no minimum balance. The $500 cash bonus requires setting up at least one recurring direct deposit of $500 or more (from an employer, government, or pension) within two months of opening.

One personal note from my own experience: the fee waiver is a real draw, but it isn't the whole picture. I found CIBC frustrating when it came to incoming Interac e-Transfers — payments would get held with no clear explanation, and sorting it out over the phone was painful. BMO took the same incoming transfers quickly and without the drama. Branch convenience matters, but so does how a bank treats money coming in — worth weighing if you'll be receiving transfers often.

- TD pairs a flat $500 cash bonus with a 12-month rebate on its $17.95/month Unlimited Chequing account. You must open the account by October 1, 2026 to qualify.

- RBC waives the monthly fee on its Advantage Banking account for 12 months and offers up to 12% cash back for three months on the RBC Cash Back Mastercard (apply by October 31, 2026). RBC's eligibility is time-windowed: permanent residents and international students who arrived within the last 12 months, or temporary workers within the last 48 months.

- Scotiabank StartRight's value is reward-points heavy rather than straight cash — the confirmable bonus is 40,000 Scene+ points on the Passport Visa Infinite card after $2,000 in spending within the first three months (a promotional, variable figure), with the Preferred Package's $16.95 monthly fee waived for 12 months.

- BMO NewStart advertises a large bundled value, with the Performance Plan ($17.95/month) fee waived for the first two years and cash/perk bonuses; it's open to anyone who arrived in Canada within the last five years.

Summary: Don't anchor on the biggest "total value" headline — those numbers stack savings, points, and conditional bonuses. Compare the guaranteed fee waiver and the cash you can actually unlock with your real direct deposit or spending.

How to Open a Bank Account in Canada: Step by Step

Newcomers can open most accounts before their credit history exists, and several banks even let you start the application before you land.

- Gather two pieces of ID. Typically your passport plus one of: PR card, confirmation of permanent residence (IMM 5292/5688), study or work permit, or a provincial ID such as the BC Services Card. Banks must accept at least two acceptable documents.

- Choose your bank and book an appointment (online, by phone, or at a branch). RBC notes service in up to 200 languages by phone or in branch.

- Apply. You'll need your address in Canada. A SIN is required for any interest-bearing or registered account, so apply for it early.

- Activate and fund. Your debit card is often printed in-branch the same day, or mailed within roughly 5–10 business days.

No Canadian credit history is needed to open a newcomer chequing account or to be approved for the bundled newcomer credit card — that's the whole point of these programs.

Summary: Two pieces of ID, an address, and (ideally) a SIN are all you need. You do not need a credit history to open a newcomer account.

Building Canadian Credit From Day One

Canadian credit scores run from 300 to 900. You start with no score at all, so the newcomer credit card bundled with your account is your fastest on-ramp.

Three habits matter most:

- Pay the full statement balance on time, every month. Payment history is the single biggest factor.

- Keep your credit utilization low — using less than about 30% of your limit is a common rule of thumb. Newcomer cards often start with a modest limit (around $1,000), so even small balances can push utilization up.

- Don't apply for several products at once, as each application can ding your new file.

Once you have a bit of income history, you can layer in tax-advantaged accounts — see our guide on RRSP vs. TFSA for newcomers to decide where to put savings.

Summary: Use the bundled newcomer credit card, pay it off in full monthly, and keep utilization under 30%. That's how a 12-month resident builds a usable Canadian score.

Why an Online Bank Makes a Great Second Account

The Big Five are convenient for branches and newcomer perks, but their everyday savings rates are low. A no-fee online bank is an excellent second account for parking savings:

- EQ Bank pays 2.75% interest on its Personal Account — but only with a recurring direct deposit of at least $2,000/month (without it, the base rate is 1.00%). It charges no monthly fee and no minimum balance.

- Tangerine and Simplii Financial run promotional rates for new clients (commonly around 4.5–4.6% for the first five months) that drop to roughly 1% afterward. Simplii's no-fee chequing account also runs a $300 cash bonus when you set up qualifying direct deposits — useful, but check the current terms.

All of these are CDIC members, so your deposits are protected up to $100,000 per insured category, per institution (see References). Spreading savings across institutions or categories is how you cover larger balances.

Summary: Keep a big-bank account for the newcomer perks and a no-fee online bank (EQ Bank's 2.75% is a strong default) for savings. Both are CDIC-insured.

Frequently Asked Questions

Can I open a Canadian bank account without a credit history?

Yes. Every newcomer banking program from the Big Five is designed to open with no Canadian credit history. You only need acceptable ID and a Canadian address. The bundled newcomer credit card is also approved without a domestic credit file.

Do I need a SIN to open a bank account?

You can open a basic chequing account without a SIN, but you'll need one for any account that earns interest or for registered accounts (TFSA/RRSP). Apply for your SIN as one of your first tasks.

Which bank gives the most cash to newcomers in 2026?

On verified straight-cash terms, CIBC (a $500 bonus plus up to 24 months of no monthly fees) and TD ($500 cash) lead. Scotiabank and BMO advertise larger "total value," but much of that is reward points or conditional perks rather than guaranteed cash.

Are my deposits safe in a Canadian bank?

Yes, if the bank is a CDIC member (all the banks named here are). CDIC insures eligible deposits up to $100,000 per category, per member institution, automatically and at no cost to you.

How long are the monthly fees actually waived?

It varies: RBC, TD, and Scotiabank waive the monthly fee for 12 months. CIBC and BMO both waive it for up to 24 months — currently tied for the longest among the Big Five newcomer programs.

References

- RBC — Banking Offers for Newcomers to Canada — Advantage Banking 12-month fee waiver, credit card offer, and eligibility windows.

- TD — New to Canada Banking Package — $500 cash offer, Unlimited Chequing fee rebate, October 1, 2026 deadline.

- CIBC — Banking Offers for Newcomers to Canada — Smart Account for Newcomers, up to 24-month fee waiver and $500 bonus terms.

- Scotiabank StartRight — Newcomer Banking Offers — Preferred Package fee waiver and Scene+ points bundle.

- BMO — Newcomer Bank Account Offers — NewStart Performance Plan fee waiver and bonus terms.

- EQ Bank — Rates and Accounts — Personal Account everyday interest rate.

- CDIC — What's Covered — $100,000 per-category deposit insurance coverage.